Global Energy Monitor’s Latest Report Misses Several Key Facts about LNG

On Monday, Global Energy Monitor, an American environmental activist organisation, published a report criticising the development of new Liquefied Natural Gas (LNG) infrastructure. Their argument against such infrastructure was two-fold; prices for renewable energy are dropping so quickly that the LNG industry will be rendered ‘unprofitable’ and that natural gas is incompatible with global goals to reduce greenhouse gas emissions.

So how do these claims stack up against credible studies and energy market forecasts? Not very well at all.

The Big Picture

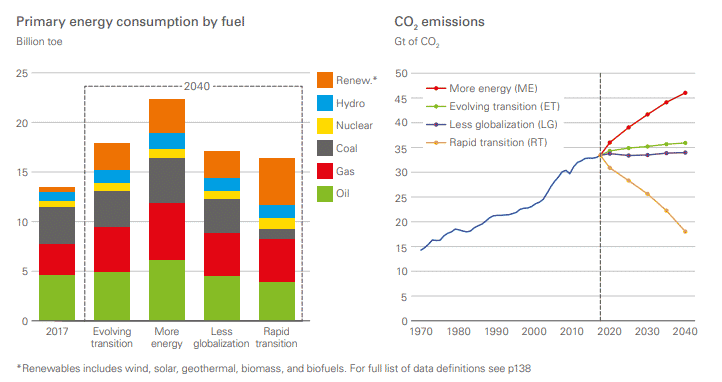

In a broad sense, the finding that the falling coast of renewables will abrogate the need for fossil fuels at anytime soon does not square with mainstream analyses.

For example, take the International Energy Agency’s (IEA) most recent World Energy Outlook. In its Sustainable Development Scenario, the IEA scenario fully aligned with Paris Agreement objectives, fossil fuels still account for 60% of the global energy mix by 2040.

Similarly, in BP’s 2019 Energy Outlook, the Rapid Transition Scenario predicts that fossil fuels generally– and natural gas specifically– will play a commanding role through 2040.

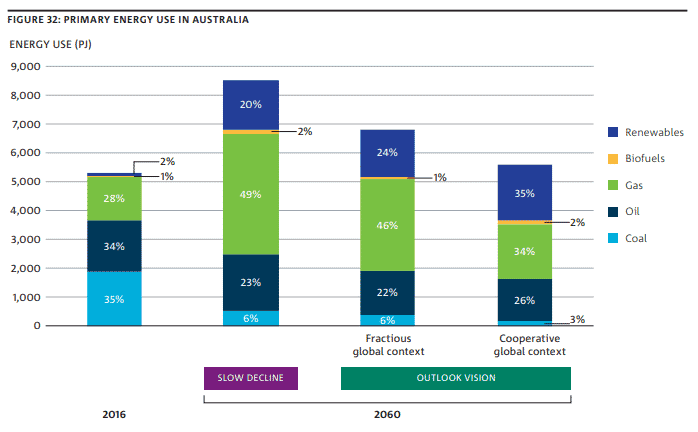

Australia is no exception to these global trends. Last month, the CSIRO published its Australian National Outlook, which mapped two scenarios for the country’s energy mix through 2050 the Slow Decline Scenario and the Outlook Vision (in the latter, greenhouse gas emissions would be reduced to ‘net zero’ by 2050). The study found that to achieve this ‘net zero’ emissions future, the share natural gas in Australia’s total primary energy mix would have to increase from 28% to anywhere between 34% and 46%.

Of course, renewables increase in this scenario too, up to anywhere between 25% and 37%– a far cry from even half of Australia’s total primary energy use.

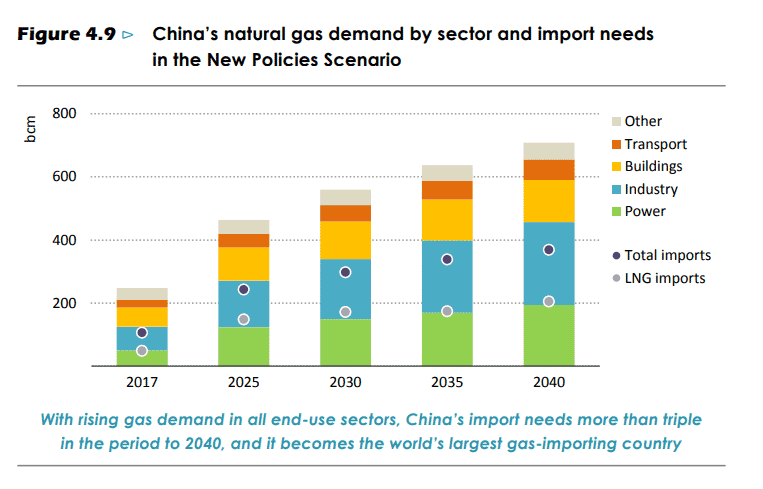

Although Australia does not stand out among global energy mix forecasts, our country has a very important role to play in decreasing global emissions – helping China, the world’s largest carbon emitter, wean itself off of coal even as its energy demand skyrockets.

Emissions

This is where Global Energy Monitor’s argument really falls apart. LNG and associated infrastructure will remain a profitable enterprise because of LNG’s emissions profile, not despite it, and this is especially true in Australia.

Why? A couple of factors are in play here:

- First and foremost, natural gas is significantly less carbon intensive than coal. While the Global Energy Monitor estimates that ‘natural gas produces about 40% less carbon dioxide than the combustion of coal,’ most experts, including The Union of Concern Scientists, estimate CO2 emissions are actually 50%-60% lower when natural gas is used.

- China is rapidly transitioning away from coal and towards natural gas in order to decrease its emissions and clean up its air pollution. These efforts have been codified in its Blue Skies Action Plan.

- China cannot produce enough of its own natural gas to meet its domestic demand.

- Australia is China’s #1 source of LNG.

- China’s dependency on Australia for LNG imports is expected to grow substantially over the next few decades. As depicted by the International Energy Agency:

To read more about China’s Blue Skies Action Plan check out our factsheet.And finally, methane emissions. A great deal of the Global Energy Monitor’s emissions concerns centre upon methane. They correctly identify methane as a potent greenhouse gas but do not include the latest research on methane leakage rates and by doing so they overstate the impact of methane associated with the oil and gas industry. The latest study on methane was published in May by the U.S. National Oceanic and Atmospheric Administration (NOAA), it found:

‘Our estimated increases in North American ONG CH4 are much smaller than estimates from some previous studies and below our detection threshold for total emissions increases at the east coast sites that are sensitive to U.S. outflows. We also find an increasing trend in ethane/methane emission ratios which has resulted in major overestimation of oil and gas emissions trends in some previous studies.’ (emphasis added)

Bottom Line: The LNG industry remains a sound investment especially as it is expected to play an even more prominent role in the global energy mix as the world seeks to decrease its greenhouse gas emissions.